Missing The Biggest Stock Market Rallies – Are They Worth The Agony For The Buy-And-Hold Investor?

I have read so many articles recently from the investment industry and the so-called financial professionals about what happens to your investment account value if you don’t follow the buy-and-hold method.

What I have learned is just how good some professionals are at making people see precisely what they want them to through the use of misleading titles, graphs, and averages. The findings extrapolated from the presented scenarios can be downright unethical when you dig just beneath the surface. For example, if you consider the emotional and financial pain, stress, and anxiety, that a retiree holding falling assets during bear markets or recessions experience, especially when an unrepentant financial industry led them to believe everything would be A-OK, it is unacceptable.

Some study titles, angles, and quotes used to make you think the buy-and-hold strategy is the only option for investors are:

- If you miss the best ten days in the stock market, you miss half of the growth.

- Why you will miss the best market days if you sell during high volatility.

- To make money in the stock market, do nothing, just hold.

- Time, not timing, is what matters.

Before I really get into the meat of this article, let me state one quick thing. I do think the buy-and-hold strategy can be a valid option for young investors with smaller investment accounts and who have a 30+ year investment horizon. But if you are nearing retirement or are retired already, you don’t have “time” on your side. During bear markets or recessions, Buy-and-Hold morphs into the Buy-and-Hope strategy, and hope should have no place in an investment portfolio. If you plan or need to withdraw capital to subsidize your retirement during this time, you will compound your problems and suffer from a “sequence of returns risk,” which is the most damaging thing to a retiree’s financial future.

So why does the financial industry do this? Well, the system is built around managing money in a way that is simple, can be sold to the masses generationally, and can leave your money in the market for 10, 20, 40+ years with minimal adjustments and all the while collecting AUM fees. To a technical trader and investor like me, AUM stands for “Assets Under Managed.” My 13-year-old daughter could do the math, put 60% of a portfolio into an index ETF, the other 40% in a bond fund, and then check on it once a year to see if it needs rebalancing. It’s not rocket science. I know investors who are paying $35,000+ a year in advisor fees, and they lost about $750,000 in 2022 following so-called ‘professional advice.’

Multimillionaire investor Jim Rogers said:

“Diversification is something that stockbrokers came up with to protect themselves, so they wouldn’t get sued for making bad investment choices for clients, and that you can go broke diversifying.”

Another reason the advisory industry pushes out content like this is that if the professionals all support it, then to the average investor, it looks like the diversified buy-and-hold method is the right and only way to manage money. But the reality is diversification is the best way to suffer from volatility and have status quo returns like every other hoodwinked investor who remains uninformed about technical analysis and asset revesting methods.

Getting back to one of the titles mentioned earlier, if you are curious about when the best days in the stock market actually happen and how it can alter your future, then you should find this article helpful.

It’s easy to think that these days occur when stocks are surging higher in a bull market, but is that, in fact, true? It turns out that it is…and it isn’t.

Chances are that in a clear bull market, whatever strategy you are using, be diversified buy-and-hold, technical analysis, fundamentals, etc., your account will be on an upswing. It’s a time when many individuals loosen the reins on the rules and opt not to lock in profits along the way, instead choosing to try and increase their returns more dramatically. Or they may neglect to set protective stops believing that they can figure it out and deal with it later when price starts to weaken. When this downturn inevitably begins to happen and is confirmed on whatever news source an investor tunes into, it is at that moment most people apply risk control measures, like a stop loss order, to protect their money. Unfortunately, by this point, it is often already too late.

I should quickly and steadfastly note that delaying protecting your position and capital is NEVER a good idea. It is ALWAYS better to make the first thing you do after entering a position is to set a protective stop and control your risk. Bad things happen, and they generally happen fast in the markets. If you are not around to exit a position, it could be very costly.

In a bear market, the answer is not so cut and dry. For example, let’s take a moment to examine the following finding:

“About 42% of the S&P 500 Index’s strongest days in the last 20 years occurred during a bear market. Another 34% of the market’s best days took place in the first two months of a bull market—before it was clear a bull market had begun.”

Source: Ned Davis Research, cited by Hartford Funds

An investor who is weathering the storm brought on by the buy-and-hold strategy during a bear market is likely to cling to these big rally days as though it were a life-saving ring. As I see it, though, the problem is that the life ring is not attached to anything. There is no dock, there is no ship, there is no land, and there is no one to pull you to safety. There is just you, bobbing away.

Will you stay in that environment forever? It is unlikely. If you can hold on long enough, the tide will eventually turn, and the stock market will turn bullish again. Your accounts will creep higher, and the day will come when you celebrate breaking even. Time will pass, and you will hit new high watermarks and think, ‘Let the good times roll’! The memories of financial ruin, desperation, fear, stress, and anxiety will fade, and the cycle will begin again.

It sounds like a fun rollercoaster ride, doesn’t it? The reality is that I believe the industry brainwashes investors, and they all have Stockholm Syndrome. But I won’t get into it here.

Let’s take a few minutes to dig deeper into the quote above to see if holding stocks during those big rally days during a bear market is worth holding on to. Given the fact that 76% of the strongest days in the stock market occur within bear markets and during the early Stage 1 bottoming phase, it should be the first red flag that what the financial industry preaches may not be the holy grail strategy they say it is.

Think about it. During a bear market, when prices are falling 1-5% per week over many months, who really cares if there is a 5 – 10% rally in the price of stocks if the price is still lower than before the bear market started. You are still losing money, and all those short-term rallies do is give panicked investors false hope that the market has bottomed and is starting a new bull market.

The same can be said for how the industry claims dividend reinvesting is a great low-risk method to build wealth. Again, nothing could be further from the truth. If an asset price plummets by 30%, is a 2% dividend payout going to make you feel richer? Does it make up for the huge decline in your life savings at a time you need it the most? Dividend stock investing is how you achieve status quo returns.

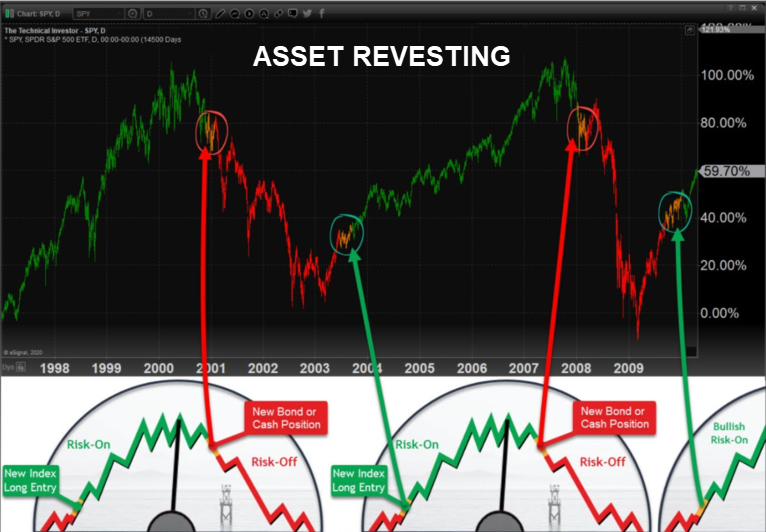

I want to take a moment to walk you through an actual investment scenario. For this example, I will assume that a $1,000,000 account was invested in a diversified portfolio of assets that tracked the performance of the S&P 500 index. The investor used the buy-and-hold strategy through the market peak of the Dot-Com peak and held through to the break-even recovery level many years later.

The Dot-Com crash began in March 2000 and lasted until October 2002. During this period, the S&P 500 index fell by approximately 49% from its peak to its bottom. In this case, the S&P 500 index did not return to its March 2000 peak until September 2007, approximately seven years later.

Assuming the same account and portfolio data from above, investors had one month, ONE MONTH, to celebrate returning to their previous account high of $1,000,000 before the bottom dropped out again. This time, the S&P 500 index dropped approximately 57% from its peak in October 2007 (a loss of $570,000) to its bottom in March 2009. This time the market didn’t fully recover to its pre-crisis levels until March 2013.

Unless you were one of the fortunate few who chose a different approach in September or October of 2007 and moved to cash or used a strategy to profit from the declining market, it took 13 years to break even. A 13-year drawdown is beyond painful – it is life-altering and nothing short of a nightmare for a retiree.

As a brief aside – if you are unsure what a drawdown is, as I have been shocked to learn that many active investors do not understand, please click this link to learn more. There are two types of drawdowns that you need to be aware of.

Fast forward to today, in the volatile Stage 3 topping phase market phase we are navigating, the peak we experienced in 2022 may not be reached again for 3, 7, or 13+ years. Capital protection and asset management are a must for investors for the next several years…unless you like afore mentioned roller coasters.

During that 13-year nightmare, there were some big rally days in the market, and the financial industry had us believing this was a cause for hope, if not celebration. In actuality, none of them mattered because they all happened when the investments were already at a loss. In fact, the only time missing big rally days makes you fall behind a little is during a raging bull market when stock indexes are making new all-time highs. Those are the real growth rallies.

Concluding Thoughts:

In short, all these bear market rally days did, was offer a glimpse of hope when there was nothing to support or sustain it. They served as a rallying cry to ‘hold on, and things will get better’ and then fizzled away to account for not much more than that. At the end of the day, did the buy-and-hold strategy work? Sure, but it took roughly 4,700 days to do so. If you are in retirement, that is a very long time to wait for income and growth…and a very long time to live in fear, stress, and anxiety.

Having been an active trader and investor since 1997, I have lived, learned, and profited through multiple bull and bear markets. I have survived and thrived in global events because I trade and invest differently from others. Through the use of technical analysis and an asset hierarchy, I identify trends, follow prices, and manage positions and risk. This is my first key to long-term success. I teach two strategies in the Second Edition of my book, Technical Trading Mastery – 7 Steps To Win With Logic.

I then take things a step further and invest differently using a style called Asset Revesting, which I deeply explore in my new book “Asset Revesting – How to Exclusively Hold Assets Rising in Value, Profit During Bear Markets, and Continue Building Wealth in Retirement.”

Chris Vermeulen

Chief Investment Officer

www.TheTechnicalTraders.com

If you enjoyed this article, please share it with others, and be sure to Join My Free Analysis and Signals Newsletter and have more articles like this delivered to your inbox.

Disclaimer: This and any information contained herein should not be considered investment advice. Technical Traders Ltd. and its staff are not registered investment advisors. Under no circumstances should any content from websites, articles, videos, seminars, books or emails from Technical Traders Ltd. or its affiliates be used or interpreted as a recommendation to buy or sell any security or commodity contract. Our advice is not tailored to the needs of any subscriber so talk with your investment advisor before making trading decisions. Invest at your own risk. I may or may not have positions in any security mentioned at any time and maybe buy sell or hold said security at any time.