Pilots, Professionals, and Entrepreneurs Should Reduce Their Portfolio Risk

Let me share with you a story about one of my clients named John, a 59-year-old retiree who was looking to secure his portfolio. John had experienced market volatility before, and it had caused him a lot of stress and sleepless nights. He came to us for a different way to manage his investments in a more conservative manner. After he reviewed our investing strategies to find out which one fit his financial goals and risk tolerance best and did the personality test, he decided to use our Consistent Growth Strategy. He felt that this strategy would help him feel more secure and avoid market volatility while producing nearly two times higher annual returns than what he was currently experiencing with his advisor.

However, just a few weeks later, John called to tell us that his son, who was a financial enthusiast, had convinced him to take a more aggressive approach with a different service. Despite our warnings about the potential risks, John followed his son’s advice, and what happened next is likely exactly what you are thinking. The market ended up declining, causing John to lose a significant amount of money from his portfolio. Now, is there anything wrong with listening to the advice of well-meaning people? No, of course not. But, as in this case, the element that John and his son forgot to account for was that the son has years to recover from investments that do not pan out. John no longer has that luxury.

Unfortunately, I see this all the time. A younger investor (and even some far more experienced ones) falls for a strategy that trades all the fast-moving stocks, is aggressive, and has a high level of risk. The issue is that everything is good until it’s not, and when the losses build, the investor quickly finds out the strategy is way riskier than he or she wanted or can stomach. But by this time, it is much too late, and the damage has been done.

Wealth Math – The Link Between Drawdowns And Age

You may not know this, but the math changes in how investing works once you are 50+. I call this “wealth math“ or lifestyle investing, and you can make more money with a lower annual return, which surprises almost everyone.

It’s important to review the investment strategy being used for your portfolio at each stage of your life to ensure that you are not taking too much risk. Doing this can help you avoid losing money and experiencing unnecessary stress. Based on our experience of talking to innumerable people, nearly all investors over 50 have their money invested in a much higher-risk strategy than they realize.

If you own stocks and bonds and are invested by way of the passive buy-and-hold strategy used by firms like Schwab and Fidelity or financial advisors in general, then you best ask them to find out how much you stand to lose during the next bear market, which is just around the corner from the looks of things. Market volatility is part of investing, but with the right guidance, you can secure your investments and achieve your financial goals without the risks and rollercoaster rides.

If you want to see the level of risk your retirement account and lifestyle have, you can get a taste of that by reading this post on the two types of drawdowns that kill investors’ retirement accounts and lifestyles.

My investment philosophy

Keep it Simple

I believe in keeping things simple and easy to understand. If an advisor is giving you information that is too complex and you don’t understand it, there are two reasons why. First, they don’t realize that you are struggling to understand. The solution – speak up. You are paying your advisor a good chunk of money, and encompassed in that fee is all the time you need to understand what the heck they are talking about. It’s your hard-earned money, and it’s your future, so take an active role in understanding what is happening to it.

Reason number two is a little more nefarious. It’s possible that your advisor is trying to prove how smart they are, which better serves their interest than yours. This tactic is often used to camouflage that your money is being spread out like peanut butter across all different kinds of stocks and assets. What this ‘diversification’ does is act like a shield. When one stock or asset begins to fall, a non-fiduciary bound advisor can easily say something along the lines of “but look at what’s happening over here” and thus distract you from what can potentially become a huge loss. If the traditional buy-and-hold diversification strategy is being used, which is a high-risk strategy for anyone nearing retirement or already retired, it is again up to you to understand what that actually means. I have found that no one cares about you or your money as much as you do, and if you don’t take the time to know what is best, then you are destined to have subpar results like everyone else.

Many of our subscribers are surprised at how easily our investing strategy can guide them with their investing decisions. I’ve heard from so many individuals – sharing how they now understand what and why we invest the way we do and how we’re providing them the education, confidence, and peace of mind that they always wanted when it comes to their investments.

My Consistent Growth Strategy newsletter can help you in two ways.

First, is that it provides detailed investment signals to follow. These trade alerts are complete with symbols, entry prices, protective stop levels, and price targets for ETFs. You can choose to simply copy these trades, which I also trade in my account.

Second, is that if you are busy, don’t know much about the markets, or just want a done-for-you solution where my trades are automatically executed in your retirement account, I offer that as well for no additional cost using a third-party autotrading broker. This is similar to the robo-advisors like Betterment, and Wealthfront, with the exception that I only charge a flat newsletter signal subscription fee and that my strategy manages positions and risk. Traditional robo-advisors use the old buy-and-hold method, while charging an asset under management (AUM) fee, which can be much more costly.

Slow and Steady Wins

I believe in conservative strategies. Our best customers are the ones who want to ensure they’ll not run out of money in the end, meaning they want to preserve their capital and generate returns to live on during retirement. They don’t care about making the highest returns in the shortest amount of time possible. They care about having the best advice that will make their money last and ensure they’ll be okay in retirement.

My investing strategy is different. I don’t believe in huge diversification, nor do I believe in holding assets that are falling in value. Because of this, investors using my conservative high-growth strategy not only reach retirement, they thrive like never before.

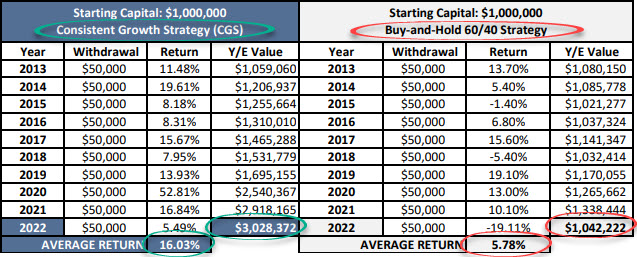

Take a look at my strategy vs. the buy-and-hold method for the past ten years for a retiree starting with $1,000,000 and withdrawing $50,000 a year. As you will see, with position and risk management (which makes for a more consistent return), investors become wealthier in retirement vs. just treading water.

Belief and Follow-Through

Finally, to be successful, you must believe in the process and have the self-discipline to follow through. If you are nearing or already retired, then the most important thing for you to understand is your new financial situation is all about capital preservation and risk management. This cannot be achieved with a stock and bond buy-and-hold strategy, so check with your advisor today to find out how your money is invested.

With the knowledge you learn, you can take the appropriate action and implement a well-designed strategy built for retirees so you can avoid all the issues and concerns most suffer from. Once you see how your goals and dreams can come true in retirement and how you will be equipped to experience them, you can take your family and friends along for the ride.

So, if you are not happy with your investment returns and are stuck having your capital plopped into the market, hoping it will generate the returns you want and need, then you should review The Technical Traders Ltd.’s investment methods and how we can help you live the life you want.

Financial Advisor Asset Revesting used for navigating client’s portfolios through several downward trends. Their assets all grew despite market volatility.

If you enjoyed this article, please share it with others, and be sure to Join My Free Analysis and Signals Newsletter and have more articles like this delivered to your inbox.

Chris Vermeulen

Chief Investment Officer

www.TheTechnicalTraders.com

Disclaimer: This and any information contained herein should not be considered investment advice. Technical Traders Ltd. and its staff are not registered investment advisors. Under no circumstances should any content from websites, articles, videos, seminars, books or emails from Technical Traders Ltd. or its affiliates be used or interpreted as a recommendation to buy or sell any security or commodity contract. Our advice is not tailored to the needs of any subscriber so talk with your investment advisor before making trading decisions. Invest at your own risk. I may or may not have positions in any security mentioned at any time and maybe buy sell or hold said security at any time.